"'Financial Shock': Mark Zandi on the Risky Loans Behind the Meltdown"

http://knowledge.wharton.upenn.edu/article.cfm?articleid=2076

Mark Zandi is chief economist, and founder of Moody's Economy.com. Moody's is one of the rating agencies that has been reported as dropping the ball in the recent financial meltdown, rating sophisticated mortgaged backed securities as AAA, or as good as U.S. Treasury bills and bonds. Mr. Zandi is in the process of publishing a book "Financial Shock" which is about the entire mess. Here is a quote from the above article:

"Well, many things surprised me. But at the most fundamental level, it was just how egregious the lending had become at the peak of the housing boom. It wasn't just simply making loans to people with low credit scores. It was making loans to people with low credit scores with no down payment, or down payment assistance. With no proof of income and just an enormous amount of risk layering that was going on. You know, I had a sense that obviously underwriting standards in the mortgage industry had fallen. I had no concept to what degree they had declined. And that's a bit surprising to me, because many of my clients are in the industry. They're mortgage companies, mortgage insurance companies; the Fannie Maes and Freddie Macs of the world. And I thought I had a pretty good understanding. I thought it was bad, but I had no understanding of how bad it really was."

Mr. Zandi closed the interview with this comment: "We still don't know -- really don't know -- how many people are being foreclosed on. No one knows. And that's not the fodder of good policy-making."

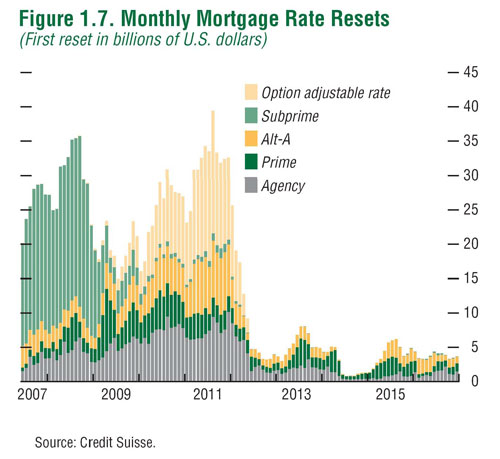

For some idea of what the foreclosure rate will look like for the near term (2008 to 2012) go to this link, which shows the anticipated increases in mortgage interest rate resets, or increases. Foreclosures will rise as these mortgages reset. The chart isn't pretty:

http://www.goodevalue.com/wp-content/uploads/2008/04/imfresets.jpg

As for Mr. Zandi's comment about the numbers of people being foreclosed on, consider this. It is anticipated that many option-ARM borrowers will face significantly higher monthly payment increases in the near future. How many? The statistics I have seen indicate that loans totaling about $30 billion will reset in 2009 and as much at $70 billion will reset in 2010. These are not sub-prime loans.

As a result, defaults are expected to double again. I think that politicians or economists who expect the housing market crises will “bottom” in early 2009 are absolutely wrong, unless there is strong government intervention to prevent these automatic resets. This event is not a surprise. In March 2008, Goldman Sachs estimated that a 15% decline in housing values would occur and that 21% of the total number of people with a mortgage would owe more than their house was worth. However, it was also estimated that if a recession occurred then there would be a total decline in the value of housing of 30% and a whopping 39% of people owing mortgages would be under water. It is now a certainty that we are in or are entering a serious recession.

I am not certain if our government will intervene until it is too late. At present, congress is working on committees of lynching parties rather than averting this looming crisis. So batten down the hatches and be prepared for a potentially rough ride for the next two or three years. However, the pessimists say it will be 2020 before all of this gets straightened out!

For more on the mortgage resets, go to:

http://letmethinkaboutthis.blogspot.com/2008/10/is-it-greed-or-stupidity.html

{kind=link}

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment